The Nuances Of Volatility

How do we measure volatility in the market? Can we really use Market volatility, the VIX or "fear gauge"? Lets go over how its measured, why traders care and value investors couldn't care less.

Hi Everyone 👋

Welcome to the new subscribers who have joined Aconomics. and If you’re reading this but haven’t subscribed, join our community! 👇

What follows is my attempt to briefly give some perspective on what volatility and the VIX really mean and why I think in most cases, the VIX is more of an interesting piece of information rather than a metric to base portfolio changes on. Lets get to it…

Volatility in the markets always spike when uncertainty increases. As retail and institutional investors try to decipher world events, from political intentions to the ramifications of every headline, the market swings and the volatility makes us crazy. Just in the last few months the Delta variant, the Chinese crackdown on their tech companies and the Taliban grabbing the reins of a whole country, I’ve decided, not to check my portfolio 120 times a day and just do it 30 times a day :)

As this events rolled in, we started hearing again about the VIX so I decided to go over:

Volatility and the VIX

A bit of History

Usability & Warnings

The VIX, Volatility Index or “the fear gauge” pops on the news every time something BIG happens or when there’s a feeling something is about to happen, but, what exactly does it mean when we read CNBC headlines like “Implied volatility warnings..” or “VIX climbs after…”?

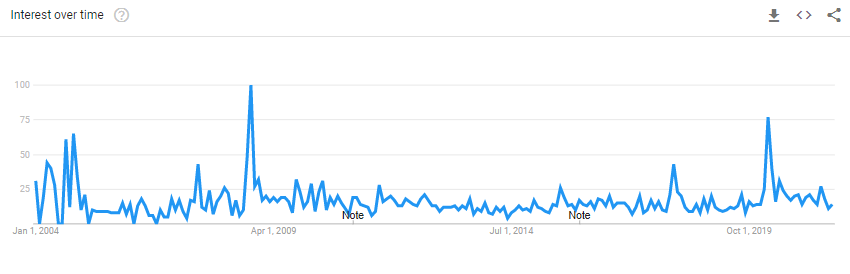

Well, according to Google Trends, a lot of people have questions, just look at the spikes in “the VIX” searches in 2008 and 2020:

Volatility is a tricky concept when it comes to the market, the VIX is used by the press without any nuance and even the creator of the VIX is perplexed about how popular his indicator has gotten since its inception.

Volatility and how we got to the VIX:

First, we know what volatility (in the market) is; volatility represents the size of the swings of an asset price around the mean price.

Second, we know that there are a bunch of ways to measure volatility and that it’s super easy to measure when we have as much data as we do (specially today).

So why is it tricky?

Well, if I tell you the volatility of the Apple stock for last week, or last year, you might be able to make a judgement call and decide if you want to hold, buy or sell and for how long. With that number, I’m just giving you outdated information that does not factor in current political situations, expected world events or market sentiment. Not very helpful.

So financial researchers came up with a solution. Because traders can't use past performance as an indicator of future performance, they have to estimate by using options. Now, implied volatility is an essential part of options trading (always has been), what was created was a volatility index.

A bit of history

In 1992, the Chicago Board Options Exchange (CBOE) who was and still remains the largest options exchange in the world, hired the Finance professor Robert Whaley to create the Volatility Index based on the work of two financial economics researchers, Menachem Brenner and Dan Galai.

Robert Whaley grabbed all the data from the CBOE, took a sabbatical from Duke University and moved to a small town near Dijon, France for 4 months until he worked out the formula for what it turned out to be the “Chicago Board Options Exchange Volatility Index” or “The VIX” and was unveiled on Jan. 19, 1993.

Basically, he created a volatility index derived from S&P 100 Index options, with the price of each option representing the market's expectation of 30 day estimated volatility.

Or, as an official description puts it: The VIX is a 30-day expectation of volatility given by a weighted portfolio of out-of-the-money European options on the S&P 500. - European options is just the name of the contract style that only allows the option to be exercised at the expiration date, not before.

Side note: Originally the VIX was based on the CBOE S&P 100 Index (now called VXO) and was changed by CBOE and Goldman Sachs in 2003 to the S&P 500 Index.

Volatility Index Usability

So now we know that the VIX isn’t as clear-cut as a “Volatility predictor”

What we see is the perception of investors buying options for the next 30 days updated daily via the price they pay, this does not mean:

The VIX can or should be used as a market timing signal, even though the VIX is generally negatively correlated with the broad market indices, this correlation ebbs and flows.

That absolute numbers mean something. Many investors thought and might still think that extreme high or low readings of the VIX are signs that the market is about to reverse. An extreme high was thought to be 35, and when reached, it triggered a buy signal. In 2008, the VIX got to 35 three times and by the third time, many investors took it as an indication that the worst was over. Not good.

The volatility is precise. Much less on the VIX that on the options of a specific stock because the options of the S&P 500 are bought by institutional investors as a hedge and they are willing to pay a premium for the insurance.

Like with any index or graph, you can find people that will draw some lines and come to conclusions but there is no indication that the VIX can consistently help anybody predict the market. So how are we suppose to use it?

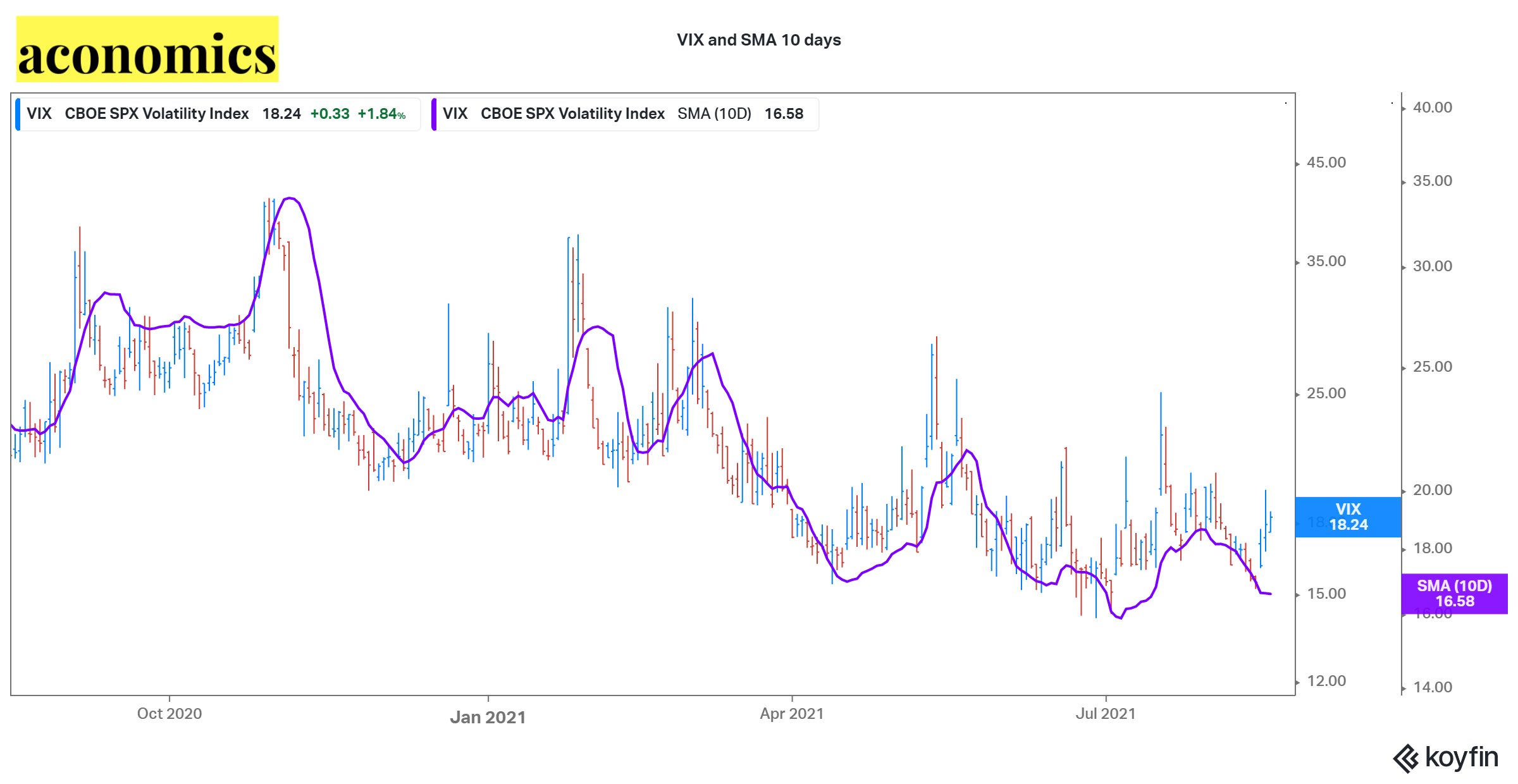

The most reasonable way I’ve seen is by Larry Connors from Trading Markets

One way to look at the VIX “is to look at where it is today relative to its 10-day simple moving average. The higher it is above the 10-day average, the greater the likelihood the market is too fearful and a rally is near. On the opposite side, the lower it is below the 10-day moving average, the more the market is too complacent and likely to move sideways-to-down in the near future.”

But even with a relative view of the VIX, its still just one more measure and as a long-term value investor, I don’t really mind short term volatility, and unless your a professional day trader, this is why you shouldn’t care that much either:

In 1929, the stock market crashed.

In 1987, the stock market crashed.

In 2008, the stock market crashed.

In 2020, the stock market crashed.

Since 1926, the stock market has returned an average 9-11% per year.

Until next time!

And again, thank you for subscribing! If you like my content, I would highly appreciate you sharing it. And if you see a typo, an error or have anything else to point out, I don’t give a f! Just kidding, please let me know in the comments or connect with me on twitter @aconomicscom :)

Disclaimer: All material presented in this newsletter is not to be regarded as investment advice, but for general informational purposes only. You are solely responsible for making your own investment decisions. In any case, transparency is paramount so my portfolio can be viewed here.